Many are curious about how to apply for an Iceland credit card, especially those planning an extended stay or relocation.

Understanding the process helps avoid common pitfalls, so this guide covers the essentials with plenty of practical, real-world insights.

Whether someone is moving to Reykjavik, studying abroad, or frequently traveling to Iceland, this article unpacks the core steps that make the experience smoother.

Why Consider an Iceland Credit Card?

Credit cards are indispensable in Iceland. If one has ever visited, it quickly becomes clear: cash is rarely used. Most places accept cards, and some even prefer them. The convenience is undeniable, particularly for visitors or newcomers adapting to local norms.

Widespread Card Acceptance in Iceland

In small towns, gas stations, and even remote tourist spots, card payments are the default.

Some travelers say they never needed cash during their entire stay. This widespread acceptance makes a local credit card even more helpful.

Need for Local Transactions

Certain services—like setting up an Icelandic phone plan or paying utility bills—often request local card details. These little administrative moments can become easier with an Iceland credit card.

Who Can Apply for an Iceland Credit Card?

Credit eligibility in Iceland hinges on specific requirements. Generally, banks look for stable residency status and verifiable income in Icelandic krona. Sometimes, just having a valid Icelandic ID isn’t enough, though it’s a good starting point.

Icelandic Residents

Permanent and temporary residents with a kennitala (the local ID number) usually have the most options.

Factors like employment history, local income, and credit score come into play. Students and new arrivals may find different requirements based on their status.

International Applicants and Non-Residents

For non-residents, options are more limited, but not impossible. Some banks offer specialized cards for short-term visitors or expats, though choices can be narrower. Usually, proof of local address and legal residence is still required.

What Documents Are Needed?

Most banks in Iceland request a consistent set of documents when considering an application. Of course, requirements do differ, so it’s wise to check with the chosen provider before gathering paperwork.

- Valid Passport – Essential for verifying identity and nationality

- Kennitala (Icelandic ID) – Makes most financial processes much easier

- Proof of Income – Recent pay slips, bank statements, or employment contracts

- Proof of Address – Utility bills, rental agreements, or official letters addressed locally

- Residence Permit (for non-EU/EEA residents) – Confirms legal stay in the country

Banks might also ask for a local phone number, though not always. Sometimes, they’ll request additional documentation during the verification stage, especially if an applicant’s situation seems unusual or unclear.

How to Choose the Right Iceland Credit Card

Selecting the best Iceland credit card isn’t just about approval odds. It’s about matching features with personal needs. Local providers often design cards for Icelandic lifestyles, with unique perks or fee structures compared to international brands.

Major Icelandic Card Providers

- Landsbankinn – Offers classic and premium cards, with reward points for everyday spending

- Íslandsbanki – Known for student and youth options, plus cards tailored to frequent flyers

- Arion Banki – Focuses on digital banking ease and flexible payment plans

- Kortathjónustan – Provides both Visa and Mastercard products, sometimes with better travel integration

Each issuer has a slightly different process. Some might require visiting a branch in person, while others support online applications.

Features available—such as insurance, points, or cashback—can shift without notice. It pays to read the fine print, even if skimming the highlights usually suffices.

The Application Process: Step by Step

The application journey in Iceland balances online convenience with bouts of paperwork. Some banks support digital forms; others expect a physical visit. The broad steps are quite consistent, though, even if the details differ.

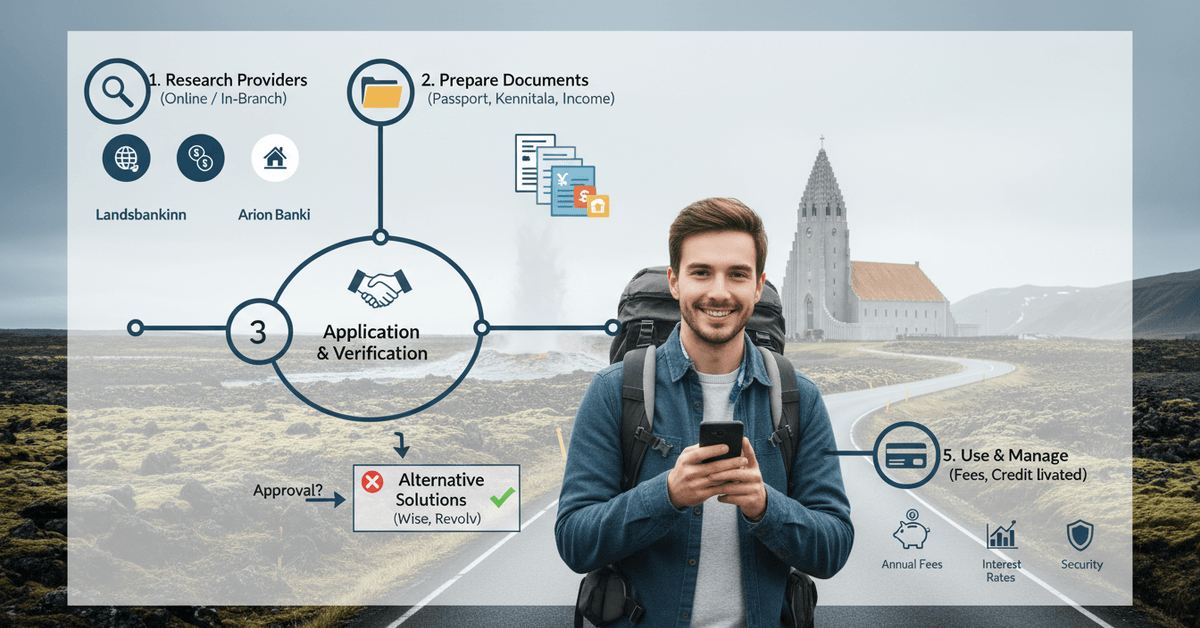

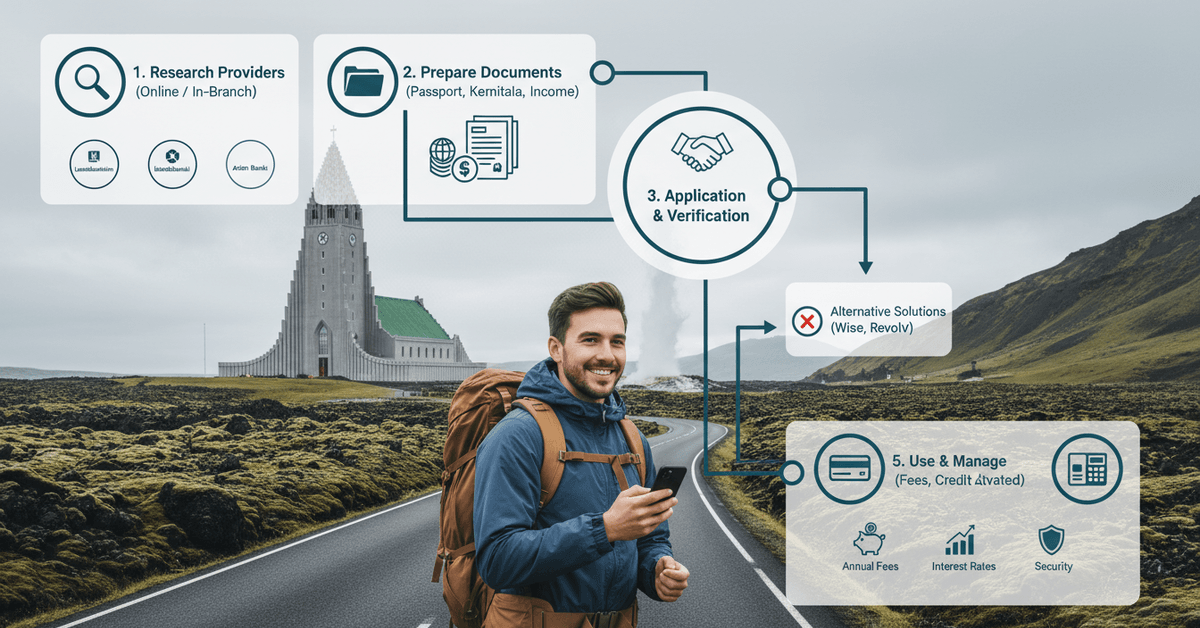

1. Research Available Options

Comparing card types and providers first seems obvious, but it’s easy to rush. Consider annual fees, foreign transaction charges, perks, and eligibility criteria. Sometimes the lower-fee option isn’t the best for frequent travelers.

2. Prepare the Required Documents

This stage often takes the longest, especially for newcomers who must secure documents from home and Iceland. Keeping originals and clear copies ready avoids delays—a small but helpful tip.

3. Start the Application (Online or In-Branch)

Some banks (like Íslandsbanki) allow applications on their websites. Others expect documents to be brought to a local branch.

4. Verification and Approval Process

Banks verify identity, review creditworthiness, and may ask for further details on employment or income. Approval times vary—from a few days to several weeks. Patience is sometimes required. Occasionally, following up with a polite call can help move things along.

5. Card Issuance and Activation

Once approved, cards are typically mailed to a local address or picked up at the issuing branch. Activation usually requires a PIN and formal ID verification. Some banks streamline this with SMS codes or digital banking apps.

Understanding Local Banking Fees and Rates

Icelandic credit cards come with fees: annual charges, interest rates, and transaction costs. Banks sometimes promote special offers, but it’s essential to check the long-term numbers.

- Annual Fee – Charged once a year; varies by card type

- Interest Rate – Can feel high compared to other European countries

- Foreign Transaction Fee – Small charges on overseas payments, something travelers notice

- ATM Withdrawal Fee – While rarely needed, it’s good to check in advance

Some applicants have mentioned surprise at the higher rates. The local banking system is relatively small, which partly explains the fee structure.

Credit Card Safety and Responsible Use in Iceland

There are real perks to Iceland’s financial tech. Credit cards have extensive protection, but responsibility is expected, too. Missed payments or high balances can impact local credit scores, which are becoming more important.

Common Security Measures

- Chip and PIN security is the norm—contactless tap is increasingly popular, but always with transaction limits

- Banks notify cardholders quickly about suspicious activity, via SMS or app alerts

- Lost or stolen cards are dealt with urgently—many banks have 24/7 hotlines

Building Credit History

For newcomers, using an Icelandic credit card responsibly over time contributes to a local credit profile. This can matter for renting apartments, securing loans, or even signing some mobile contracts in the future.

Alternatives to a Traditional Iceland Credit Card

For those who do not qualify right away, prepaid cards or international banking apps can bridge the gap.

Some people have used Wise, Revolut, or N26 until their local accounts are set up. These alternatives don’t always offer the same acceptance as an Icelandic card, but they help during the transition.

Conclusion

Iceland credit cards for international applicants offer exceptional application accessibility, genuine competitive banking benefits, authentic fraud protection, comprehensive worldwide merchant acceptance, proven, reliable financial services, and excellent customer support.

Apply for your Iceland credit card today as an international applicant with complete confidence, knowing your thorough preparation and clear step-by-step understanding will help you effectively secure approval.